Another month, another update. A few random comments.

Good Reads/Listens/Watches

- GCC featured on national news (link). Loved the accompanying blog post.

- “As I explained to ABC, if there was any magic we had it was that we were willing to live like college students longer than it is socially acceptable to do so. Along with earning a good income and staying healthy, this allowed us to aggressively save.”

- The ability to pretend we’re still college students is basically our biggest superpower as well.

- Wrote a follow-up article on how boring investing should be. Worth a read (link).

- Those who understand investing (GCC, Buffett, Bogle, Fama, etc) repeatedly try to beat the simplicity of investing into our heads:

- Step 1.) Regularly dump money into index funds (preferably in tax sheltered accounts).

- Step 2.) Ignore the news about impending calamities and shoddy advice contradicting Step 1.

- Step 3.) Wake up 40 years from now a rich individual, much richer than had you violated Steps 1&2.

- The great paradox of investing is that you can’t beat the market, but instead should focus your efforts on things you can control (savings rates, tax efficiency, etc). I love the absolute simplicity of my current two-fund portfolio which will eventually turn into a 3-fund portfolio.

- If you need any more inspiration to keep it simple, here is Buffett on index funds (link).

- Those who understand investing (GCC, Buffett, Bogle, Fama, etc) repeatedly try to beat the simplicity of investing into our heads:

- “As I explained to ABC, if there was any magic we had it was that we were willing to live like college students longer than it is socially acceptable to do so. Along with earning a good income and staying healthy, this allowed us to aggressively save.”

- Wealthy Accountant on the difference between debt and wealth (link).

- Reminds me of lessons learned from reading the Richest Man in Babylon over a decade ago:

- When you are in debt the clock works against you. Every morning when you wake—weekends, holidays, sick days, birthdays and work days—you are already behind. The mortgage, credit card, car loan, et cetera, all tacked on interest the second after midnight. Long before you rolled out of bed and poured your first cup of coffee you need to work to pay the interest before you have money for food, clothing, shelter or entertainment.

- Here is the secret if you weren’t paying attention:

- Saddled with debt the clock works against you. Tally up all your debts and calculate the interest accruing daily. Now you know why it’s so hard to get ahead. It isn’t your wage; it’s you! You forgot to do the math and now the universe is teaching you a valuable lesson. If you survive. More on that in a moment.

- Here is the secret if you were distracted by the bright lights:

- If you have no debt you start each day with a clean slate. You own nothing to anyone as you start your day. You still need to take action to cover your daily needs, but at least you are not behind before you start.

- The secret again is:

- Without debt, but with investments, interest accrues to your account before the coffee is brewed. Dividends were earned, wealth created.

- The secret again:

- Investments in interest baring accounts build slowly, yet daily. Investments in index funds means virtually every purchase by every man, woman and child added something to your nest egg. Each sale added to the coffers that pay you dividends. Each sale adds value to the companies you own in the index fund. Each sale is part of the wealth creation process.

- Reminds me of lessons learned from reading the Richest Man in Babylon over a decade ago:

- The Finance Buff is quitting his well paying day job to focus on the blog & consulting income full time (link).

- He has an interesting write-up of his post-transition health insurance options and selection process here.

- Lest anyone worry about me doing the same, my blog pulled in exactly $2.10 in revenue last month while incurring $9 of domain name & hosting expenses.

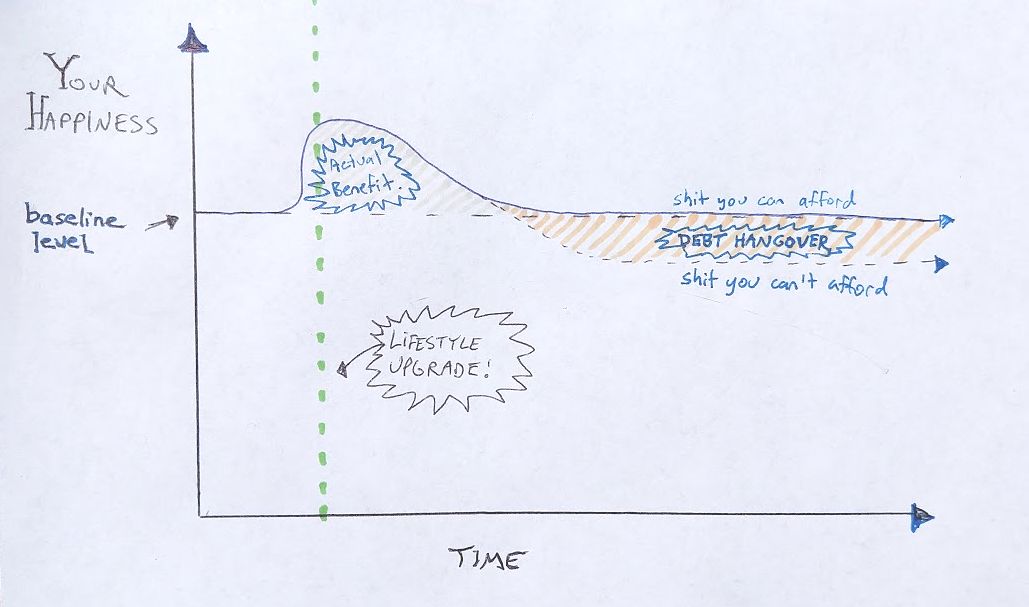

- Bogleheads forum discussion on the “why” of high savings rates (link).

- My answer of “why” is answered by this picture in MMM’s most recent blog post on hedonic adaptation.

- I can’t think of any purchase that would meaningfully & permanently increase our level of happiness.

- Any trinket that we could bring into our lives would give us a momentary bump in happiness, which would fade as the novelty of the new purchase wares off.

- I can’t think of any purchase that would meaningfully & permanently increase our level of happiness.

- My answer of “why” is answered by this picture in MMM’s most recent blog post on hedonic adaptation.

- Freakonomics interview of famous surgeon/author Atul Gawande about the state of the healthcare system & steps forward (link).

- EconTalk episode on the astronomical costs of many cancer drugs and the dysfunctional incentives in that market (link).

- Grim WSJ video on running out of money in retirement and a few states feeble efforts to avoid this through auto-enrolling them in Roth IRAs (link).

- There are simply no easy answers to the impending retirement crisis. Have no money in your 60s? Go back in time 40 years, spend less, be smarter with taxes, and invest your savings in low cost index funds (after Bogle invents them in 1976).

{kind=link}

Life

- My body broke:

- (Re)broke my nose playing basketball (first time was in high school playing basketball two decades ago).

- Basketball is a young man’s game and I’m no longer a young man. I should probably stop playing.

- My friend & neighbor set it in his kitchen (he’s a radiologist, so it’s all good).

- Woke up the morning after to a very swollen elbow. Bursitis. Doc friends said to take Ibuprofen which helped.

- (Re)broke my nose playing basketball (first time was in high school playing basketball two decades ago).

- Continued to use our moviepasses:

- Great: A Quiet Place.

- Good: Love, Simon.

- Meh: Ready player one.

- Snow in early April.

- WILL THIS WINTER END!?!?!?!?

- Looks like it ended late-April.

- WILL THIS WINTER END!?!?!?!?

- Began our 7-year-old tradition of a “marathon in a month”.

- Over a 30 day period, we have our kids run a mile a day (2 miles a day for the older kids). For some crazy reason (we’ve been doing it for so long), our kids think this is a normal activity and don’t complain.

- It’s one of our favorite family traditions. We stole it from a neighbor we met during the PhD. It’s fun to have a shared, common goal among all of our family members. We love it because it helps to get their energy out and teaches them to challenge themselves physically.

- After each mile, our kids go home and mark off their mile on a countdown chart. After the last mile, we have a party. Usually with other families if we are doing it with them. We give awards, have popsicles, etc. Fun times.

- Figured out the solution to smelly climbing shoes (or smelly anything for that matter).

- Bamboo charcoal

- $15 for 8 bags of the stuff here: https://www.ebay.com/itm/262963229451

- It sounds totally scammy, but it’s legit.

- Bamboo charcoal

- To wrap up the semester, I taught an optional personal finance lecture to my students.

- Got an email after the fact from one of them: “Just wanted to say thanks for yesterday’s lecture. Debatably the most important lecture in my four years here. I have always been a big saver so I look forward to the next few years of maxing on my investments.”

- Only about 20% of my students showed up.

- It’s odd that such a potentially helpful lecture to students about to graduate is blown off by 80% of them.

- Being a professor is weird. Most students don’t want to be there. I don’t blame them; I didn’t want to be there for many of the courses I attended over my 12 years of college. But it’s nice to look back on the semester and realize that you’ve made an impact on a few students.

- Summer bowling is upon us.

- One of our favorite summer activities. Our 4-year old leapt for joy when we told him that bowling season had arrived.

- If you have kids, sign up for free summer bowling at https://www.kidsbowlfree.com/.

- Has worked for us in multiple states so far.

- Kids are free. Parent passes are something like $25/year total for both parents

- We own our own bowling shoes.

- https://www.bowling.com/products/classic-kids-rental.htm

- https://www.bowling.com/products/classic-mens-rental.htm

- https://www.bowling.com/products/classic-womens-rental.htm

- One of my old college buddies claimed that investing in a pair of bowling shoes produces one of the highest returns on investments of any investment on the planet. While I initially thought he was crazy, I have since learned of the wisdom of that statement.

- This friend has the highest net worth of any of my friends, by a large margin. He knows a good investment when he sees one.

- One of my old college buddies claimed that investing in a pair of bowling shoes produces one of the highest returns on investments of any investment on the planet. While I initially thought he was crazy, I have since learned of the wisdom of that statement.

- At lunch, one of my colleagues shared something he learned on a TV special debunking flat earth types. I’m not interested in debunking idiocy (like the belief that actively managed mutual funds are a good idea), but I thought the experiment on the TV special was great. The experiment that they ran was to shine a laser flat across a lake and have a boat sail away. For each mile it traveled, it marked on a white board the level of the laser. If the earth is curved, the laser will go up on the white board as the boat travels away and follows the curvature of the earth. Can you figure out how much the laser increases if the boat is 1 mile away? 5 miles away? 10 miles away? The only parameter you need is the radius of the earth, which is 3,959 miles. The four of us professors (three of which are former engineers) were geeking out at the solution to this problem. Our solution mapped exactly to what they found on the show.

Answer to the curvature of earth brain teaser.

Answer to the curvature of earth brain teaser.

Happy marathon in a month participants (Frugal children #2 & #5).

Happy marathon in a month participants (Frugal children #2 & #5).

Frugal child #1 climbing. Kids are naturally excellent at climbing, as they have a very high strength to weight ratio. This is most evident when trying to do the monkey bars as an adult alongside my kids. Monkey bars used to be easy. Not so any more. One of the more impressive athletic feats I’ve seen in the past few years is frugal child #3 swinging continuously on monkey bars at a public crossfit-like facility for 5 minutes straight until his hands gave out from blisters.

Frugal child #1 climbing. Kids are naturally excellent at climbing, as they have a very high strength to weight ratio. This is most evident when trying to do the monkey bars as an adult alongside my kids. Monkey bars used to be easy. Not so any more. One of the more impressive athletic feats I’ve seen in the past few years is frugal child #3 swinging continuously on monkey bars at a public crossfit-like facility for 5 minutes straight until his hands gave out from blisters.

The morning after breaking my nose, I awoke to an elbow the size of an orange. The picture does not do it justice..

The morning after breaking my nose, I awoke to an elbow the size of an orange. The picture does not do it justice..

This month’s finances

- The good:

- Stuffed another $9.25k into 403b+457.

- Stuffed $5.5k into backdoor Roth.

- The bad/abnormal:

- High deductible plan strikes back with $786 in bills. All medical visits occurred months ago.

- $346 mole removal & $83 biopsy came through.

- We should have done this for less money in Denver, but after receiving the quote in Denver we called home to see what the price would be and our doctor’s office implied that it would be similar. They were wrong. Over $100 cheaper in Denver. Lesson learned: have moles removed at the free skin screening dermatologist in Denver in the future.

- The fact that the dermatologist had a cash price ready for the procedure should have been an indication to me that 1.) they knew what they were talking about, and 2.) they were competitively priced.

- It’s amazing the delay between service and payment. It’s no wonder why our healthcare system is going to bankrupt our country. People can’t make informed decisions about procedures because it’s a 6-month-long opaque battle between your doctor and insurer before you get your final bill. Doctors don’t understand prices. Insurance companies don’t understand prices. There is no hope that the healthcare market can function properly without a well functioning price system.

- Luckily our doctor understands that we have a high deductible plan and consciously tries to avoid unnecessary expenses for us (unneeded X-rays, etc). We appreciate that about him and wonder why it’s not the norm for any medical doctor to be mindful of prices when recommending procedures. I suppose when the perceived (or actual after-insurance) price of a procedure is $0, consumers rationally demand the kitchen sink in tests & treatments.

- We should have done this for less money in Denver, but after receiving the quote in Denver we called home to see what the price would be and our doctor’s office implied that it would be similar. They were wrong. Over $100 cheaper in Denver. Lesson learned: have moles removed at the free skin screening dermatologist in Denver in the future.

- $175 pneumonia dr office visit + xray.

- $93 asthma medicine.

- $89 strep test.

- $346 mole removal & $83 biopsy came through.

- $407 AirBnb expense for our portion of 3-day cabin rental at a lake over the summer with some undergrad friends.

- 3 guy roommates married 3 gal roommates. Between the 3 couples, we now have 14 kids. Should be a fun adventure.

- $290 life insurance premium on $1M, 15Y policy (10Y remaining, after which we’ll self insure).

- High deductible plan strikes back with $786 in bills. All medical visits occurred months ago.

Full version is downloadable here (link).

{kind=link}

Footnotes:

- Don’t lend money to friends/family.

- I lazily approximate home value as my historical purchase price.

- I have a 15Y mortgage; which results in a faster rate of repayment. The true cost of the mortgage should exclude repayment of principal, which I show above.

- $20 internet and $0 cell phones as described here.

- All expenditures at Costco & Walmart are classified as “Food at home” for simplicity (even if it’s laundry detergent, clothing, etc).

- I prefer Vanguard funds but my employer offers Fidelity instead.

- Nobody knows the perfect asset allocation. Just pick one and run with it. Use a target date retirement fund as a benchmark if you want some guidance (link).

- My low portfolio expense ratio is the primary reason why I don’t hold target-date funds, which have expense ratios anywhere from 0.16% to 1%. I can achieve a much lower expense ratio on my own due to Admiral shares, etc. And it’s not hard. Plus, a DIY portfolio allows one to tax-loss-harvest more easily.

- ETF’s are a pain to own relative to holding index funds directly. You have to deal with bid-ask spreads as well as the inability to buy partial shares. With a simple index fund, you don’t have to deal with either of these issues. I am currently invested in VTI b/c it’s $10/year cheaper than VTSAX in my Saturna HSA.

- The one blight in my expense ratio analysis is my 529 plan. The underlying Vanguard fund is almost free to hold (0.02%), but the high administrative fees bring the total cost of holding the fund to 0.30%. I abhor fees and would likely avoid 529 plans if I didn’t get to deduct up to $10k of contributions per year on my state return, saving myself $700/year in state income taxes.

- The only other administrative cost not captured by my expense ratios is a $19/year administrative fee for my HSA at Saturna Capital ($15 per transaction + 4*$1/dividend reinvestment).

Disclaimer:

This site is for entertainment purposes only, as disclosed here: https://frugalprofessor.com/disclaimers/

Can I just say again how much I love your blog? Please don’t let the cost of the site deter you from writing. You are teaching a lot of eager readers through your posts! I wish I knew this stuff when I was in college, but its hard to grasp at that age when you don’t have bills or a full-time job with benefits. Maybe you can make it mandatory to your students so they are forced to see for themselves how invaluable this information is =]

Thanks for the feedback. Hopefully the blog is useful.

I’ve been following your blog for a number of months now and really appreciate your writing style. Its very logical and enjoyable to read – plus you’ve got a number of great tips.

I’ll be graduating with a degree in engineering here in a couple of months and I’m ready to turn up the heat on my savings rate!

Congrats on the engineering degree! Those degrees are certainly not a walk in the park. Post graduation, remember: avoid lifestyle creep, stuff tax-advantaged accounts (specifically to avoid the 22%+ brackets), invest in index funds, and enjoy the ride.

Thanks for posting about the kids free bowling. I did a cursory check and there is a bowling alley within biking distance which participates. Although, I’m not sure if my 5 year old (our oldest) could bowl quite yet. I’ll have to check it out and see how it goes.

Great monthly update otherwise. Boring investments are good!

Score on the participating bowling alley within biking distance. We went last night (the first day our bowling alley participated), and had a blast. Our kids’ feet have grown so we placed an order for more bowling shoes online last night.

We signed up for that and the Kids Skate Free programs this week. We are looking forward to an awesome summer!

Didn’t know about the kids skate free program. Googled it but looks like no participating places near us. Bummer.

Love this blog! Again, I really appreciate the first section of the monthly updates. Marathon month is a great idea!

I wish I could take credit for the marathon in a month. I simply stole it from some friends who were cooler than us.