Another month, another update. A few random comments.

Good Reads/Listens/Watches

- Prof G interviews NYU finance professor Aswath Damodaran about the GameStop frensy (link).

- TLDR; prices are asinine and will come back down to reality sooner than later.

- WSJ article on the mastermind behind the Gamestop/Reddit madness (link).

- Here’s his Reddit post history, including snapshots of his $46M portfolio as of Jan 28 (link).

- Somewhat relatedly, I’m troubled by the proliferation of undergrad day traders. It seems that almost every undergrad I talk to has a Robinhood account and is day trading options. While I applaud the excitement about investing, I abhor the get-rich-quick mentality and the complete detachment to investing fundamentals. Surely these students would respond by calling me a “boomer” who doesn’t get it. Perhaps they’ll end up with a $46M portfolio next month….

- Aswath literally wrote the book(s) on valuation. In the podcast, he mentioned that he estimates equity markets are currently 10-15% overvalued (if my memory serves me well).

- David at OchoSinCoche has an interesting series of posts on how he’s funding college for his six children (post1, post2, post3).

- His posts are a good reminder to me that our 529s are severely underfunded (given that I haven’t exceeded the annual state income tax deduction funding limit of $10k/year).

- If I’m remembering correctly, here’s his proposed subsidization plan. It seemed pretty reasonable to me:

- 100% subsidization of tuition for first 7 semesters (at reasonably priced school; if Harvard, the difference is on them). The 8th semester is left unfunded due to a tax reason that I need to look more into.

- Any scholarship money would be pocketed by student.

- 100% subsidization of (dorm + cafeteria equivalent) room and board for first year, 75% for second year, 50% for third year, 25% for fourth year.

- 100% subsidization of tuition for first 7 semesters (at reasonably priced school; if Harvard, the difference is on them). The 8th semester is left unfunded due to a tax reason that I need to look more into.

- I really enjoyed seeing the cash flow analysis surrounding having multiple kids concurrently in college. I hadn’t seen that before.

- He computes the present value of the parental subsidy for his six kids to be $300k. Relative to the $65k we currently have saved for our 5 kids, it’s evident we’re underfunded (even though we have 17% fewer kids). His posts inspired me to think harder about whether I want to divert any future contributions from taxable brokerage accounts to 529 accounts even after exhausting my $10k/year state income tax deduction limit. His posts also inspired me to think harder about the cost sharing arrangements with our kids.

- Reader poll: what is your planned cost-sharing arrangement for your kids’ college expenses?

- Looking back, my folks footed the bill for my first 1.5 years of college (of the twelve I attended). After that, I was self sufficient thanks to going to a cheap school (plus grad-school scholarships) and having summer jobs that paid pretty well. I think it was a pretty decent agreement.

- I have friends who are footing 100% the bill for the ivy’s. $75k/year*4 years = $300k per kid for 100% funding. Ouch. I’m not generous enough to do that. Mercifully, I don’t think my kids are shooting for the ivy’s, though admittedly we’re a few years off.

- Dr Fauci discusses candidly with the NYT (podcast) what it was like working with Trump (link).

- I finally ended up pulling the trigger on the complete Reel Rock package at Vimeo (link).

- I’ve gotten through several films and they are great. However, many are available for free on RedBull’s website (link).

Life

- It snowed 14 inches in a 24-hour period which shut the town down for a few days (the elementary school was shut down for three days; the university was shut down for two). Even though we live in the midwest, the plowing infrastructure is really weak so people were unable to leave their homes for a few days.

- We ventured out a quarter mile (to Costco), got stuck, and had to push our way out. Others on the road got more stuck and we helped dig them out. The experience reinforced my irrational desire to buy a Cybertruck — the most hideous (but practical) vehicle ever designed. In the interim, my 2010 Corolla + 2012 Sienna + bikes will have to suffice.

- A ***minor*** problem with the Cybertruck is that it won’t fit my entire family (seats 6; I need 7). I’m currently working out ways to safely strap a child to the roof.

- I continued to bike to work, though they didn’t plow a quarter mile of the trail for some incomprehensible reason. I took a minor fall or two at walking speed trying to navigate that portion of the trail.

- We ventured out a quarter mile (to Costco), got stuck, and had to push our way out. Others on the road got more stuck and we helped dig them out. The experience reinforced my irrational desire to buy a Cybertruck — the most hideous (but practical) vehicle ever designed. In the interim, my 2010 Corolla + 2012 Sienna + bikes will have to suffice.

- I have a brother-in-law with a

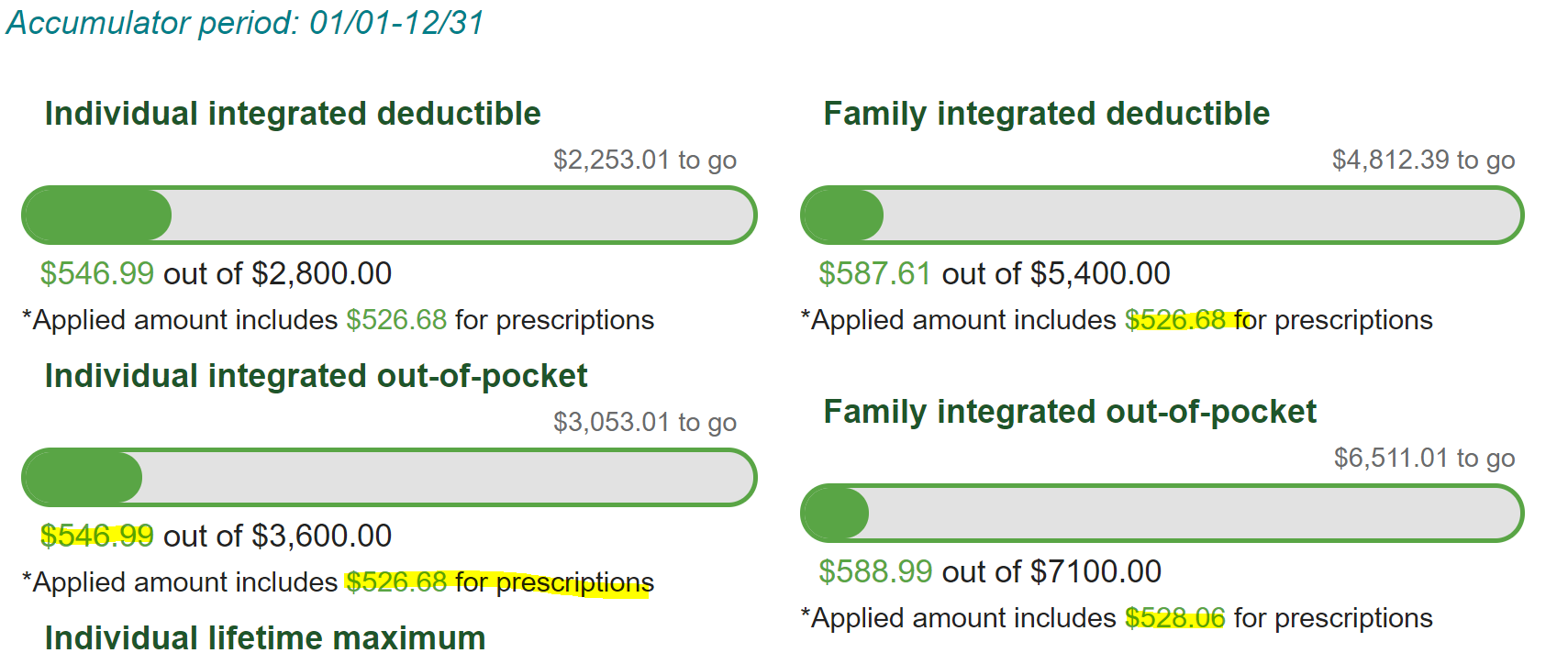

healthyaddiction to board games. Every time we get together, he brings about 30 new games to teach the family. He owns well over a thousand. A few years back he taught us the game Century Spice Road (link). I instantly loved it and bought it years ago. For some reason it sat unopened in our closet for years until this past month. It’s similar to Splendor, which is also a good game that we bought in 2015. - The healthcare prescription arbitrage is alive and well in 2021 with some previously unvetted prescriptions. Basically, my insurance company gives me full credit for prescriptions even if a manufacturer’s coupon is used. Depending on the sequencing of transactions this year, this loophole has the potential to save us about $5k on healthcare this year. Unfortunately for me, I can’t stave off all doctor’s appointments until hitting the deductible/OOP max, so the arbitrage unfortunately won’t result in $0 medical expenditures this year. Sequencing matters.

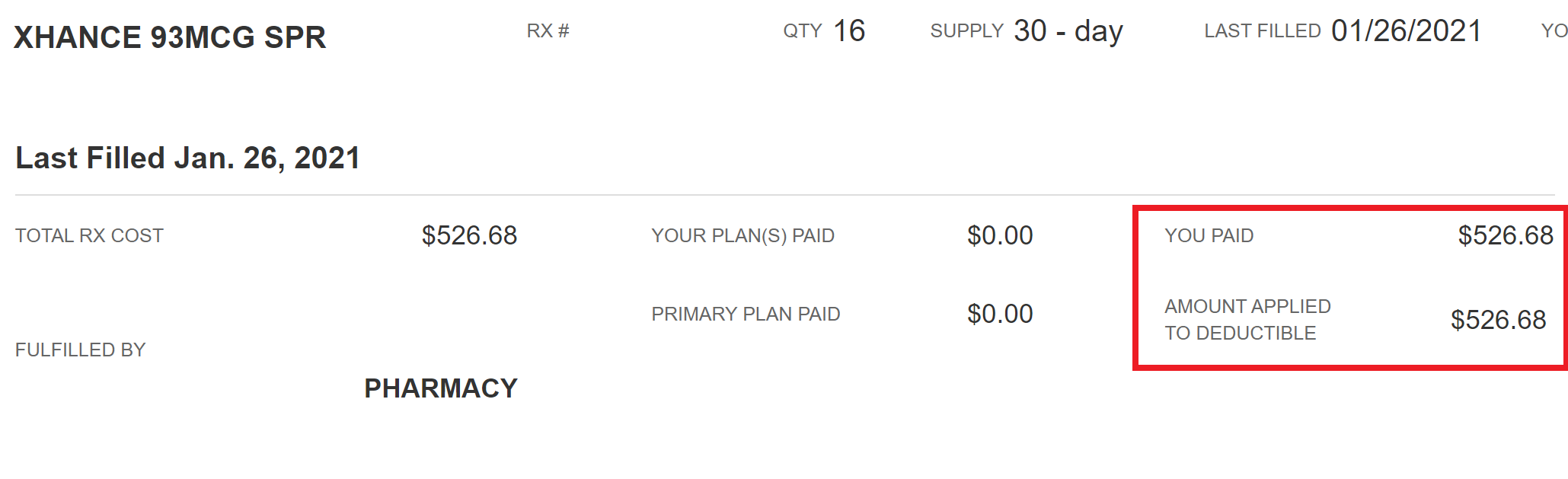

The prescription arbitrage is alive and well in 2021. I filled a $526.68 prescription, paid $0 for it thanks to a manufacturer’s coupon, and got the full credit for the drug on our healthcare deductible. It’s such a bizarre system that I don’t pretend to understand the underlying economics at play here.

We bought snowshoes for $20/pair at Costco a few years back but hadn’t needed to open them until this storm. They worked fine. Our dog was not a fan of the powder (she’d sink to her belly on her skinny stilt legs) and learned pretty quick to simply follow our tracks. The unfortunate thing is that following our tracks involved lots of her stepping on our snowshoes. It took about an hour to get our snow gear on and the kids lasted about 7 minutes in the snow before wanting to go back inside.

Winter wonderland. FC1 is collapsed in the snow somewhere in that picture.

Mrs FP almost broke her back helping to stack FC4’s snowman (FC4 did the ball rolling). FC4 was proud of the lightning scar.

Puzzles are a crowd favorite during the dead of winter. What a great investment these are. Ravensburger makes the best (link).

Post-Christmas acquisition of Mermen Ken by FC4 using her own money. This is a classic example of “stuff begetting more stuff.” For Christmas, Mrs FP got FC4 a mermaid Barbie doll. For the ensuing 20 days, I heard incessant begging from FC4 that mermaid Barbie needed a merman Ken to be involved in “love triangles.” Finally, we caved.

It appears that I am forever doomed to Barbie Ken + mermaid product recommendations on Amazon. I hadn’t been planning on it, but long-haired hippy Ken might be my next impulse purchase thanks to Amazon’s insidiously powerful algorithms. He’s pretty dreamy.

Speaking of dreamy, I’m doing my best Kenny G impersonation above to impress Mrs FP. It didn’t work. Perhaps it had something to do with my gangly body in smelly long underwear from bike commuting.

FC1 has played the clarinet for a few years at school. They give free instruction, so I’ve been a fan. In her band this year, there was an oversupply of clarinet players so they sent her home with a school-issued saxophone. The saxophone is louder than the clarinet.

This Month’s Finances

- The good:

- Still employed…

- Filled a bunch of tax-advantaged buckets (IRA + 529 + most of HSA).

- The bad/abnormal:

- $95 purchase of 24 climbing movies.

- $7.94 Barbie Dreamtopia Merman Doll.

Full version downloadable here (link).

{kind=link}

Footnotes:

- Fidelity unambiguously has the best HSA on the market. $0 admin fees + $0 expense ratio funds.

- I lazily approximate home value as my historical purchase price.

- I have a 15Y mortgage which results in much larger principal payments than a 30Y mortgage. Since principal payments are simply transfers from one pocket (assets) to another (debt reduction), I treat such cash flows as savings.

- ~$0 cell phones described here.

- All expenditures at Costco & Walmart are classified as “Food at home” for simplicity (even if it’s laundry detergent, clothing, medicine, toys, etc).

- Nobody knows the perfect asset allocation. Just pick one and run with it. Use a target date retirement fund as a benchmark if you want some guidance (link). If you prefer to DIY (as I do), then a three-fund portfolio is great (link).

- My low portfolio expense ratio is the primary reason why I don’t hold target-date funds, which have expense ratios anywhere from 0.16% to 1%. I can achieve a much lower expense ratio on my own due to Admiral shares, etc. And it’s not hard. Plus, a DIY portfolio allows one to tax-loss-harvest more easily.

- ETF’s are slightly more annoying to hold relative to index funds. With ETF’s, you must deal with bid-ask spreads as well as the inability to buy partial shares. With a simple index fund, you don’t have to deal with either of these issues. Bogleheads discussion here (link).

- I continue to own VTSAX rather than FZROX and in my taxable brokerage account because it is more tax efficient due to lower capital gains distributions. Bogleheads discussion here (link).

- The one blight in my expense ratio analysis is my 529 plan. The underlying Vanguard fund is almost free to hold (0.02%), but the high administrative fees bring the total cost of holding the fund to 0.29%. I abhor fees and would likely avoid 529 plans if I didn’t get to deduct up to $10k of contributions per year on my state return, saving myself $700/year in state income taxes.

- CA’s 529 plan has the lowest expense ratio US equity index fund of any in the US (link). I’d have 100% of my money here if not for the state tax deduction I receive in my own state.

- I own one share of Berkshire Hathaway (B Class) for the sole purpose of getting 4 free tickets/year to Berkshire’s annual meeting.

- I bought 100 shares MoviePass for $0.0127/share to be able to tell my students that I held a stock that went to zero. So far, the stock price stubbornly remains above zero.

Disclaimer: This site is for entertainment purposes only, as disclosed here: https://frugalprofessor.com/disclaimers/

That is quite the snow storm! Looks like fun.

We’re planning to pay for four years for our two kids (2 and 5) at our state university which is about $120k total per kid as of now. We have about $160k in 529s so hoping to close that $80k gap with market returns exceeding inflation in the next 15 years. If it doesn’t we’ll cash flow the difference or push community college for the first two years which would reduce the cost significantly.

Funding a reasonably priced state university seems like a great strategy. As does superfunding the 529 like you’ve done. I need to think more seriously about doing so.

Community college can indeed save a ton of money. Our high school has a pretty good AP program, so there’s a decent chance our kids can shave a semester or two off of school if they decide to go that route.

I’m curious what other readers are funding their 529s at. We have one kid (sophomore) and he has $160k+. Enough for 4 years at the flagship state college. If he gets in one of the “elite private universities” that we approve (school and major), we will consider funding this from our taxable funds.

Philip,

Congrats on $160k for the one kid! That’s really impressive!

I’m not sure I understand the question. Are you asking the level of current funding per kid (and thus the budgeted prestige of the school)? Or are you asking the desired level of future funding?

I like your plan of 100% funding at state school. Sounds reasonable. Do you have any cost sharing arrangements in place?

I guess I’m interested in 1.) cost sharing arrangements with kids + 2.) proposed budgets per kid (with implicit ceiling on spending)

I’m interested in what the expected balance of 529 plans per kid other readers are targeting. From other blogs I read, most folks target funding the 529 enough to give their kid a fully paid 4 year BS degree debt free at an in-state university. I started saving when my boy was 1 year old but the market grew faster than I expected so the balance is exceeding my target (it’s at $168k today and we still have 2 years to go).

We’re doing fairly well so decided not to do cost sharing. I did share with my kid the balance of what he has. I told him if he graduates early, decides to go to a cheaper school or otherwise graduates without spending it all, he can keep the difference (some of the $ is in a trust). I tell him the balance is his money upon graduation and he’s welcome to use the remainder to go backpacking in Europe, buy a car, use it for grad school, etc. The string is that he doesn’t get the balance unless he graduates. If he gets accepted to a “prestige” school that we approve, we are willing to pay the additional amount to cover a 4 year program so he basically gets funding beyond his current balance. It’s the carrot being used to let him try for these programs since we can afford it. We’re comfortable with this arrangement because of his personality. If he was less responsible and less studious, we would have a different arrangement.

Congratulations on having so much saved already! I’d say that’s a good problem to have.

I’m playing catchup on the 529, but my target is to save exactly up to what I need, and no further. I will never even get close to $168k for any single kid, I think.

In your case, if your child doesn’t use it all, you could still roll it into a 529 for any future grandkids (with some gift tax/generation skipping issues) or even for some continuing education for your self.

I agree with David. You’re in a tremendous situation here. Congrats!

David and I have 400%-500% more children than you, so we’re compelled to be a bit less generous. I can’t imagine a world in which I’d pay full freight to any Ivy, but maybe my views will change some day.

To the extent that parents can cash flow their anticipated college expenses, I think it’s somewhat rational to have $0 saved in a 529 to preserve the optionality of money. For the FIRE crowd, a more rational approach would be to have the PV of their expected parental contributions saved up. It sounds like you’re in the latter camp. I’m somewhere between $0 and 100% PV funded. Simply plagiarizing David’s analysis, I’m around 25% funded at the moment = $65k currently saved / (David’s $300k PV answer * 5/6).

In light of this discussion, I’m considering superfunding a 529 to catch up. The benefits are obvious: avoiding taxes on growth. The costs are too: less flexibility once the money is in a 529.

Great discussion. Congrats again Phillip!

We’re very thankful our boy will be fully funded for college, thanks to a great bull run.

I will mention that this overfunding was mostly due to shifting 529 funds from one kid to another. We kick started saving for our 2 kids very early to capitalize on tax free growth as early as possible. Over time, it became pretty obvious our autistic daughter won’t be going to regular college as she’s still non-verbal even today at age 14. We don’t have any obvious programs we want to send her to using the 529 so it all goes to our boy as he will very likely us it all since about half of the $168k is in a UTMA (in hindsight, a bad decision). I guess my message is to plan prudently but adjust accordingly.

Thanks for sharing Phillip. I agree with your conclusion to “plan prudently but adjust accordingly.”

I wish it snowed like that in VA… I relocated our family when my boys could barely walk from south central mountains in PA (lived about a 5 minute drive from a ski resort) and now it’s a big deal if we get 3-5 inches and it seems to usually melt within ~48 hours

My college plan is likely worse than yours and we only have 2 kids

Route #1 – they can pretty much pay for themselves like we did (I think my parents helped with ~5k for my 4+2) hoping the buy in helps them care more despite knowing damn well I had little/no idea about loans until i learned they wanted their money back and didn’t care that young strength coaches are broker than broke despite working ~75 hours/week

route #2 – dream/pray/hope/vote?! for free college in ~10-15 years

route #3 – same as above for scholarships

route #4 – cash flow it when we get there assuming my queen and I will be filthy rich when they move out (I sometimes wonder why my friends without kids aren’t retired already)

route #5 – ?!?!?! maybe an inheritance/universal basic income will pay for it? and an obnoxiously big truck?! (need a safe vehicle for that 2-3 inches of snow ~48 hours a year)

Joking aside, I’ve done the math and we will have invested a pretty penny in private K-12 for them (we live in one of the worst school districts in VA) assuming nothing changes over next decade or so which hopefully will be a better investment than higher ed…?!?!?!

Glad to hear that I’m not the only one that doesn’t have all of the answers yet!!! Hopefully your dreams/prayers/hopes/votes come to fruition!

We plan to fully fund tuition and room & board capped at reasonable good in state school status BUT only if the following happen: The student applies for 50 scholarships during their Junior and senior years of high school. My parents made me the same deal and I wound up getting 9.5 semesters of college paid for plus extra for spending money. I changed majors and went five years. My folks considered that my “job” in high school and so I only had to work during the summer, not the school year.

This is a brilliant approach!!!!!!!!! Thanks for sharing!!!!!

Did the scholarships you received conditional on attending a certain school, or did they allow you to go wherever you wanted?

If your children get scholarships, is the agreement to pay for any unfunded amount? Or do they pocket the scholarship (a-la-David at OchoSinCoche)?

I had some of both – I ended up receiving two full tuition scholarships but obviously couldn’t go to both schools. I didn’t get to pocket the scholarship money, I’m the oldest kid so the college money might have been needed by my sibling but she also applied for so many scholarships that her undergrad was fully funded. My parents ended up sitting pretty and we both graduated with no debt. I hated having to apply and write so many essays at first, but then you can start to tweak them and the effort needed is less and less. Most of the applications returned $0 because someone else received it, but obviously it worked out ok.

Thanks for sharing your story!!!!! I think your story is a cautionary tale to having too much saved in a 529 plan (because it’s not readily jettisoned to non-college expenses in the event of generous scholarship receipts).

You’ve certainly given me a lot to think about! I’m discussing our future plans with Mrs FP right now and I appreciate you sharing your experience!

Late response, but you can withdrawal the amount of the scholarship penalty free from a 529. You will have to pay taxes on the earnings, but not the penalty so it essentially turns the 529 into a tax deferred savings vehicle. I’ve got three kids and, though they are young, all seem to be headed down the college track. We’ve got 529s for them and we’ve decided that they aren’t “their money.” It’s all “our money” that we will gift them for college should they need it to fund a degree as long as our conditions are met. 1) You apply for scholarships. 2) You have a plan for college. (I’m ok with changing majors to fine tune an education – heck, I did that moving from Chem E & BioChem to Chem E & Food Science, but if you have no clue, there are cheaper ways than college to figure it out). 3) You stay on track to graduate.

My husband and I both graduated with no school debt (mostly by grants and scholarships) and I’d like to give my kids the same experience, but it’s not going to be a hand-out.

I appreciate the response Cat! I’ve learned a lot from you and I appreciate this added detail. This penalty-free withdrawal of 529 funds for scholarship money certainly helps to reduce the “overfunding risk” of 529s. I’ll certainly keep that in mind as I make these important college-funding decisions!

Nice snow storm! It’s been dry here. Less than 1 inch for the entire month (driest January on record)! Temperatures have been warm-ish (January average was -1.5 F), especially in the hills above the inversion (usually 10 to 20 degrees warmer at our house). Perfect snow biking conditions – trails are so firm you could ride a mountain bike!

We have $12k saved in a 529 for our 2-year old. No state tax here so not as much incentive to use the 529. I like ochosincoche’s cost sharing plan. I haven’t though too hard about the details, but tentatively planning to have enough in a 529 for a few years of tuition + room and board. I paid for my state school undergrad through a full tuition scholarship, living at home, and working. My grad school was covered with a cost of living stipend. I realize we can’t bank on our kid(s) earning the same type of merit-based scholarships, but it’s also hard to save a huge sum of money in a 529 we may not need. My wife had tuition covered/discounted because her dad worked at the university she attended. If you stay employed at your university, what kind of perks do your kids get if they attend?

The FAFSA is quite a puzzle. Low AGI parents qualify for a fair amount of aid or at least subsidized loans. This is especially true when parents have more than one student in school simultaneously. However, it takes serious planning because of the Prior-Prior year policy. Since most of our assets are in retirement accounts, it’s not unreasonable to think that by the time our child is ~18 (and we’re FI), we could stop working and have a very low AGI. I need to do some more research to understand how the 529 fits into these FAFSA calculations. Of course, there are ethical considerations with this strategy. I don’t know how old your kids are, but there’s a lot to think about if you’re considering FI in the years they are approaching university! I look forward to seeing some of your spreadsheets 🙂

(The paragraph spacing got screwed up in this comment and WordPress isn’t allowing me to fix it. Sorry in advance for the incomprehensible sequence of words that follow. I’ll put this ______________ to denote a new paragraph)

I forgot to include the usual “sorry-to-Ken-from-Alaska-for-complaining-about-a-wimpy-midwest-winter” disclaimer when talking about our January weather!

______________ < 1 inch during January is crazy! Hopefully February + March don't overcompensate. ______________ A friend of mine has a dedicated fat tire snow bike. For now, I'm sticking with the good ole' slickdeals carbon mountain bike. It's done well enough, though admittedly it didn't handle the 14" very well. ______________ I'm in the exact same boat with your 529 logic (not wanting to end up with a boatload of money that is costly to jettison for other purposes). At my current university, the tuition benefits are very modest for my children. Other Universities, however, are unbelievable. U Chicago, if I understand it correctly, covers 95% of faculty's children's tuition anywhere in the country. Notre Dame + Clemson are also quite generous. I'm sure there are many others. I had a friend once who was looking at a move to Notre Dame and the tuition benefit was a big factor. ______________ I agree entirely about the wonky economics surrounding the FAFSA (e.g. home equity isn't penalized so you have a strong incentive to pay down the mortgage to "hide" that wealth). The prior-prior year policy is similarly weird. I agree entirely that there are some perverse incentives and questionably ethical strategies that one could employ. Justin at Root of Good has kids a few years older than mine. He's a smart guy so I'm looking to see how he'll handle this. I know that he's very much in the take-what-you-qualify-for-and-ethics-be-damned camp (some of his family members are on Medicaid, they get reduced price internet for being "poor" despite being worth $2.5M, etc).

HI – great article as always. In response to the question – my parents were gracious enough to make a deal with me in that they paid for my undergraduate college, and then I would pay it forward by paying for my kids’ undergraduate college tuition/expenses. So I am definitely planning to fund their undergraduate years. I personally attended Trinity University, which is a small private school down here in Texas – so to be fair I will need to be prepared for a school such as that. My kids are currently 8 and 4. I used to contribute actively to 529s, but stopped doing so after reading an interesting article about 529s on go curry cracker blog. My current 529 balance is approximately $80K. I am definitely not anti-529’s, but I am currently not actively funding them at this time, and am planning to also utilize funds from taxable accounts (in addition to what will have as balance in 529s in 10-14 years).

I think the scholarship application idea is tremendous idea – and I am filing that one away and will surely implement it.

Thanks for sharing your experience!

I just looked up the “cost of attendance” to Trinity University. $45k/year. Ouch! My undergrad is running $20k/year for COA and the school I teach at is $25k/year.

GCC has definitely shaped my thinking than any other blog author. I’m glad to hear that his posts have had a similar impact on you. I remember the article you are mentioning. I made a comment on it. Basically, I commented that since I have 5 kids, the idiosyncratic risk that one or two doesn’t want to go to college doesn’t absolve me from the near-certainty that most will. That calculus is a lot different with 1-2 kids.

I similarly love the scholarship idea and am likely going to borrow it as well.

I also went to Trinity University in San Antonio, Doug! It was a fantastic experience, one I appreciate even more teaching at a flagship state institution. I hope I can pay it forward for my kids and support a similar experience to my own.

As always, thanks for the rich information in your post. I very much appreciate the transparency in posting your financial updates (I know that makes me a financial voyeur). I tend to use your posts as a data point against my own progress. I especially like how “simple” your portfolio is. In comparison, my financial life could definitely use some pruning. Your blog has become one of my pleasant stops on my visits around the web, thank you!

Regarding your reader poll: I have two kids, one a high school sophomore, and one in her freshman year in college (what a disappointing ride that’s been for them this year, especially after 18 years of her parents talking up the college experience … but, adapt and overcome). My deal is 100% funding for a state school, they take on half of the tuition difference for a private school. I live in VA, so the state is blessed with excellent state schools, and my oldest did me a solid by deciding to go to the best school in the state. It’s still expensive (about $26k this year), but not crippling. I used to fret about it when she was younger as I watched my savings rate fall way behind the tuition inflation rate. But once she actually matriculated, I find that I am just very grateful to be in a financial position to give her this gift.

Quick question: My income is approximately the same as yours, but I find that l exceed the income contribution limits for an IRA. How are you getting around this?

Thanks for comment!

The financial voyeurism is indeed weird. As a public university employee, I’ve come to appreciate that there is no secrecy since my salary is already public. I’m just taking it a tiny bit further and showing the merits of deliberate frugality + tax optimization.

I like your funding agreement with your children; particularly the 50% responsibility for anything in excess of the state school. I might plagiarize this.

The Roth IRA contribution occurs via the “backdoor”: https://www.bogleheads.org/wiki/Backdoor_Roth

It’s most cleanly accomplished with $0 Trad IRA balance before hand. If so, it’s dirt simple:

1.) Dump $6k into Trad IRA

2.) Immediately convert to Roth IRA (using “Transfer” feature in Fidelity or this link at Vanguard: https://personal.vanguard.com/us/ConvertToRoth

3.) You’re done. When you file your taxes, be sure to properly fill out form “form 8606” with your taxes. You’ll get a 1099-R when you do the conversion. You’ll owe $0 taxes on the conversion if you convert immediately. Check out my draft “book” in the header of the site to learn a bit more. Search the doc for “backdoor” to find the section.

If you don’t currently have $0 in a Trad IRA, try rolling it into a 401k to remedy that situation.

You can contribute to your 2020 IRA (not a typo) until April ~15 of 2021.

The “backdoor” roth is also mentioned in this post: https://frugalprofessor.com/hierarchy-of-savings/

Thanks for the shoutout. You got all the details on how I plan on doing things. Of course, it’s still a plan and subject to change!

That’s a lot of snow. We live in northern Virginia and every decade or so we get dumped on a bit. I think the last time was 2015 with something like 25 inches in one storm. This past week it dumped about 8 or 9 inches over two days. Kids had a blast sledding in our front yard, although a couple nearly got concussions (I exaggerate!) when they hit some of the large tree trunks.

Love the Puma/Costco socks in your saxophone picture. I have some on right now!

Thanks again for the great college expense analysis. You’ve given me a lot to think about.

The Costco Puma socks are the best socks I’ve ever worn. We have them in all sizes for all people. They are the (almost) exclusive sock of the FP household. In the winter, we mix it up with the Kirkland Signature wool socks.

Sledding can be sketchy. On a trip to UT over Christmas, our kids and I did sledding standing up. A poor man’s snowboarding experience. It was a blast and made me feel slightly guilty for never having taken my family skiing/snowboarding. I’ll have to remedy that one of these years, although a single day would easily set our family back $1500. It’s hard to justify that expense.

Yeah, I feel slight guilt not doing skiing/snowboarding trips. But the expense does seem high. If we lived somewhere like Colorado or Utah, I’d find it much easier to stomach.

I seem to recall that the last time I looked I found that the FAFSA is not just about AGI, but also savings and investments (excluding retirement accounts). I did some rough calculations based on the FAFSA worksheets and found that it doesn’t take much savings to run the “expected family contribution” up to 100%. I think the aspiring FIRE people that read this blog need to realize that. It means that, unless something changes drastically with the FAFSA, even if they stop working, their personal savings is likely going to totally disqualifying their dependent student from any federally subsidized loans or need based money. If that’s the case, then I don’t see how anyone can have the plan to only fund part of their child’s education. How is the child going to pay for the other part? It seems like the child’s only options are going to be private loans with terrible terms, or working part time (and going to a cheap enough school where part-time work will have any chance of covering the cost of attendance). Does anyone have a solution for this problem?

Thanks for the thoughtful response Scott. Check out Root of Good’s post here: https://rootofgood.com/pay-for-college-while-retired-early/. He’s a thoughtful writer. I haven’t read this post in years but will do so again thanks to this renewed discussion.

I just filled out my second FAFSA with my oldest and taxable accounts definitely count “against” you. We qualified for unsubsidized Stafford Loans that my daughter could take and Plus loans that I could take, somewhere around 5%/year. To open myself up to subsidized loans and Pell grants, it seems I’d have to drop both my income and savings way down, shuffling money into my mortgage and tax advantaged accounts. Neither seems worth it to me.

Thanks for the response David!

If I had access to the elusive “mega” backdoor Roth, it would essentially entirely replace any future contributions to a taxable brokerage account. In such a world, I could conceivably have $0 in a taxable brokerage account. Particularly if I liquidated the account now to pay off the mortgage. Or alternatively dumping some of it into a donor advised fund.

This reinforces my desire to bring the mega-backdoor Roth to my institution even more……

Wow that spreadsheet is very detailed is that all manual entry or automated to pull account balances? Seams to be allot of work to keep up with all of that data entry.

Im new here just started following. I did not see any sort of life insurance in your spreadsheet which in theory if you invest correctly that would become your self funded life insurance coverage. But…I was wondering if you had any simple spreadsheet that analyzes different type of life insurances Vs. Investment.

Example I have a Custom Whole life $250 a month for $120k (increasing over time) coverage but now im looking to cancel that policy and go with term $20 a month for $250k coverage (30 years) & invest the remainder of $230. I would love to see how investing $230 within a safe interest vehicle would compound over time compared to staying on course by keeping $250 invested in to a custom whole life policy plays out.

I’m an Excel monkey, so spreadsheets are fun to me. Personal Capital does 99% of the work for me. I just scrape from their website.

I pay $290/year for a $1M term policy. It was a 15Y term policy when I first got it. I’m probably 7Y into that term now with 8Y to go. Once it expires, we’ll self insure.

I’m not much of an expert with insurance, but the near unanimous consensus from what I’ve read suggests that term is the way to go. Insurance salespeople will try to convince you otherwise because their livelihoods depend on you drinking the kool aid. The (near unanimous) consensus is to separate insurance from investing products. With the savings achieved with term (vs whole), you simply invest the difference. Preferably in tax-preferred vehicles.

BTW, risk-free vehicles are producing negative real (inflation adjusted) returns. Going forward, it is a crappy time to be an investor.

Yes I think your right im only 3 years in to my Custom whole life but im on the verge of cancelling it mostly for the reason its either or a death or life benefit if someone dies you can not collect both the death benefit & the cash value which make me think why combine the 2? I might as well separate investment vehicle & Insurance vehicle.

The sales rep is calling me on Friday to convince me why I should keep whole life but I want to arm myself with a good compounding interest spreadsheet so I can say. If i go term and invest the difference myself in 10 years @ X interest i will have $xxx vs if I invest in term ill only have $xxx.

I also need to arm myself with the cash surrender value that I have lost to this point. I been investing $300 for near 3 years with a cash value of only $3,300 & a death benefit if $120k, big mistake.

I also have a couple term life policies totally about $650k for 30 years (about 12 years into one, 8 into the other) and pay a total of $600/year. When the sales insurance guy calls, make sure you remember the sunk cost fallacy: sticking with a bad deal because you’ve already put value into it. Good luck on the call.