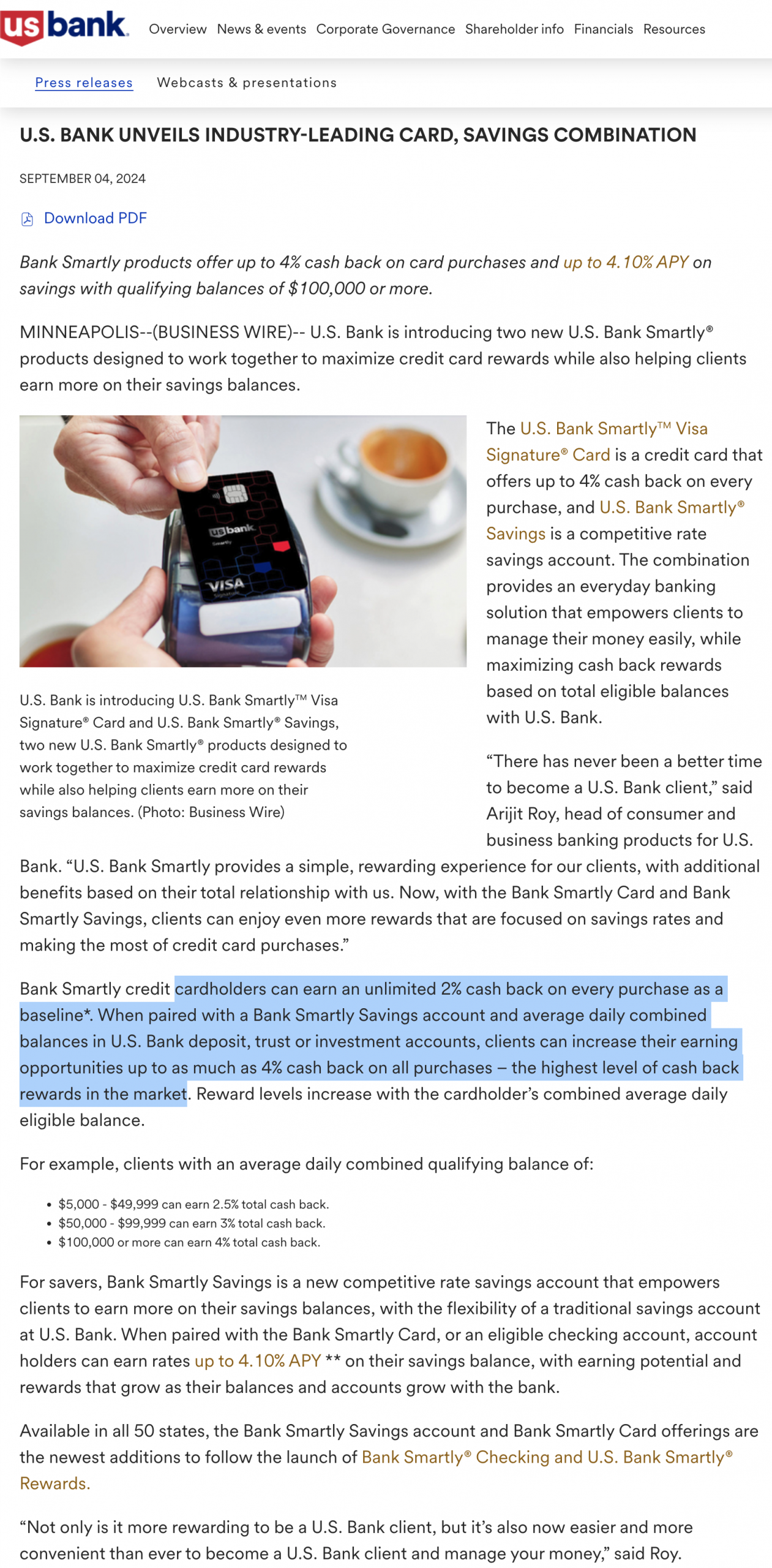

On September 4, 2024, US Bank made big news with their announcement of an “industry-leading” card purported to earn 4% on all purchases (screenshot below). The card started accepting applications on November 14, 2024. In the ensuing 8.5 months, it has been almost comical to behold the meteoric (and inevitable) implosion of this card.

US Bank is not deserving of your banking, investing, nor credit card business going forward. There are far superior — or dare I say “smartlier” — non-US Bank options for banking, investing, and credit cards, and I’ll outline each of the superior options in this article from the perspective of a finance professor. This article outlines the same advice that I give to my students and children. It’s the same advice I follow myself.

(Lack of) Disclaimer

I don’t make money from this blog. There are no ads. I don’t get credit card referrals. I make about $50/year from Amazon affiliate links but that is less than the cost to run the blog (~$150/year). I maintain this blog because I like writing about finance.

What Was the Bait and Switch:

- Per the news release above, US Bank promised $100k of eligible investments (e.g. stocks, mutual funds, etc) would count to earn the 4%. They have reneged on this over the last few months for existing cardholders. New cardholders can only earn the 4% if they park $100k in a checking account, which essentially means the implicit annual fee of this “no annual fee” card is the $4k/year opportunity cost on the uninvested cash (who sits on $100k of uninvested cash in checking, by the way).

- Per the news release above, US Bank promised 4% on all purchases. They have since excluded taxes, insurance payments, and education.

- Per the news release above, US Bank promised unlimited 4% on all purchases. They have since backed this down to $10k per billing cycle.

If US Bank had half a brain when designing this card, they could have foreseen the obvious shortcomings:

- $100k of self-directed buy-and-hold investments in a self-directed brokerage fund generates no revenue for them. In fact, it’s a money loser when considering the administrative costs of recordkeeping (tax forms, customer service, etc).

- 4% unlimited cash back is comically unsustainable in a world with ~2.25% swipe fees and was ripe for abuse (federal tax payments, etc).

“Smartlier” non-US Bank banking solutions:

I think that Fidelity’s Cash Management Account (CMA) offers the best checking/savings account available (with a few quirks), far superior to any other product I’m aware of. I wrote a blog post on the details here: https://frugalprofessor.com/the-ultimate-guide-to-fidelitys-cash-management-account-cma/

“Smartlier” non-US Bank investment solutions:

It is difficult to communicate how important it is to choose the right investment firm. From my experience, Fidelity is the best brokerage out there. They offer a great investment options (arguably far too many), but importantly to investors they offer many low (or no) cost index funds like FZROX (0% expense ratio total US stock market fund), FSKAX (0.015% expense ratio total US stock market fund), FZILX (0% expense ratio total international stock market fund), and FTIHX (0.06% expense ratio total international stock market fund). Importantly, there are essentially zero account maintenance fees on brokerage accounts, IRAs, HSAs, etc.

Similarly, Vanguard — the pioneer of low-cost investing — offers many good investment options such as VTSAX (0.04% expense ratio total US stock market index), VTI (0.03% expense ratio total US stock market ETF), and a suite of very low-cost target date funds such as VFIFX (0.08% expense ratio target date fund).

As far as putting my money where my mouth is, our ~$3M portfolio is invested in a simple two-fund indexed portfolio across the above Fidelity/Vanguard index funds (70% domestic, 30% international). Our DIY $3M portfolio incurs ~0.01%/yr in fees, or ~$300/yr on a $3M portfolio.

US Bank’s investment platform is as bad as I’ve seen in my life. Only a truly misinformed individual — the only ones US Bank has any hope of attracting — would choose to invest with US Bank.

“Smartlier” non-US Bank Credit Card Solutions:

For unexplained reasons, Bank of America has been paying me 5.25% cash back on most transactions (Costco, Amazon, Walmart, Sams, Delta, United, etc.) for almost a decade. The primary caveat (among several) is that you need to park $100k at Merrill Edge to earn these elevated rewards. If you add an Ultimate Cash Rewards Card or Premium Rewards Card to the mix, then your worst-case cash back would be 2.625% — not bad for tuition payments, tax payments, etc.

I have no love for Bank of America nor Merrill Edge, but I tolerate them because they reward me with 5.25% cash back on every transaction.

If you don’t have $100k to park at Merrill Edge or if you don’t want to deal with BoA, then the no-nonsense and no-annual fee 2% Fidelity credit card is probably your best bet. I have had this card (starting with its predecessor — a 529 card) for 20 years now. Key features:

- No-nonsense 2% cash back on all purchases.

- No foreign transaction fees.

- No annual fees.

- $100 TSA Precheck / Global Entry credit every 4 years.

My eldest child just turned 18, and the Fidelity credit card was the first (and perhaps only) credit card I recommended for her. What a great card.

Wrapping it up:

With its ineptitude and bait-and-switch tactics, US Bank is undeserving of your business. You can do much smartlier by avoiding them entirely.

Comic relief:

My kids are watching The Office for the first time. Just last night, they watched the “golden ticket’ episode which was all too reminiscent of US Bank’s idiotic behavior over the past year.

The rabbit hole gets even deeper, if you look on Reddit there are different sub tiers of the card depending on when you signed up. It appears that if you signed up within the first week of the card being available, you are grandfathered on having 100K in savings, business accounts, or investments. However, if you signed up after the first week or two that the card was offered, you now have to keep that hundredk in checking, making this a $4,000 annual fee card.

A $4k annual fee credit card is arguably the most dumbly(TM) offering in the history of credit cards.

I’m confused. I just looked at my most recent transactions and I’m still getting the 4%. I don’t think I’ve missed any notifications from US Bank telling me that they are changing MY RATE.

I don’t see anything in this article about you being notified that they are changing YOUR 4%?

https://www.reddit.com/r/CreditCards/comments/1mbsg7m/usbank_smartly_cc_nerf_is_here/

https://www.bogleheads.org/forum/viewtopic.php?p=8457490#p8457490

Your letter will come. Mine came last night.

I’m just frustrated with the US Bank’s bait and switch tactics over the last 8 months after their arrogant initial claims.

I’m fortunate to be one of the ones receiving the “good” version of the nerf letter, but I have friends and readers (who I recommended the card to) receive the “bad version of the nerf letter yesterday. Even though I received the “good” version of the nerf letter, I have no faith the terms will remain favorable for more than a few more months.

I just think US Bank should be held accountable for their bait and switch tactics (and terrible brokerage), 8 months after applications opened on their self-hyped card. Even though I’m still on the “good” list, I regret ever recommending the card to friends/readers/students.

This does not seem to be accurate, or at least it’s more complex. I signed up months after the card became available, and the letter I got tells me that investment accounts still work for a qualifying balance.

The nerfed card still works for my spend patterns. If I got the “only checking accounts for qualifying balances” letter, I’d be ACATS’ing my funds as soon as the change went into effect.

I realize its not available anymore, but are you still using USBAR?

Yes, but this looks doomed as well: https://www.doctorofcredit.com/u-s-bank-to-make-negative-changes-to-u-s-bank-altitude-reserve-travel-transfers-1%C2%A2-per-point-instead-of-1-5%C2%A2/

Bad day for US Bank cardholders yesterday….

Looks like I’m going to go crawling back to BoA…

I got my bad letter last night, too. No love. I had to read it three times to believe it. They should have grandfathered us. I’d been reconsidering what a bank could do in customer appreciation; hah! 😒

My condolences. If it’s any consolation, I think us “good letter” folks will be dumped in a matter of weeks…

Ugh – thanks for even more “good news”…

When it rains, it pours!

Citi Double Cash (2% cash back) is another solid, straight forward card, if you don’t do a lot of international travel.

I have that card and agree that it’s good. That said, I’d give Fidelity the edge for $100 travel credit & no FTF. Certainly not life changing features, but enough for me to tip the scales to Fidelity on this one.

Unfortunately I wonder if US Bank’s bait-and-switch will pay off for them. They obviously wanted to boost their investment business, and they got that. How many people will just leave their investments there even if they stop using Smartly? And those that don’t will probably pay a steep transfer out fee.

I’m unsure how many will stay. It seems most of us that are informed are pretty fed up…

Sorry to hijack with unrelated topic to this thread.

But would you please write about taking on Stablecoins and investing Crypto sector? so we won’t miss the train, or at least have better understanding in this area.

Thanks

I don’t understand anything about crytpo and am generally pretty skeptical about it. That said, I’ve been proven wrong over the past 15 years since learning of its existence. Given my ignorance & skepticism, I don’t own crypto nor do I think it is worthy of discussion.

The short explanation of crypto is they all effectively function as money transfer tokens. How much would you pay for a Western Union token?

“Stable coins” are almost entirely pegged to some other currency for value and are very analogous to Western Union tokens.

There are more technical possibilities, however, I’m not aware of any widely adopted technical solution built on the technology. Just Western Union tokens and speculation.

This hurts my head. Thanks for trying to teach this dinosaur.

I vaguely understand the mechanics, but I have no framework to value a currency.

Unfortunately, US tax laws make using crypto outside of a hedge for inflation difficult and tax tracking intensive. Although I think that will change within the next 10 years. Texas recently passed a bill that allows for gold as a valid currency alongside the dollar, I dont see why a US sponsored stablecoin wouldnt be far behind.

Crypto’s main benefit is being decoupled from central government. Happy to go into more details. but it tends to follow the same rules as forex currency exchange or securites at the moment.

Stablecoins are intended to store something similar to fiat without a bank. useful for places were the desired fiat is not easily available. Like countries whos own currency is volatile and unreliable.

It will be interesting to see how this plays out over the next few years….

I haven’t gotten my notice, but hoping I will get the good nerf. I also have the USBAR and I happened to see the nerfing on DoC as well. I have avoided the BoA other than the unlimited cash back due to the quarterly limit on the 3%/5.25% card, but I may just need to start collecting several of the cards for different purposes to get around the $2,500 quarterly limit.

For now, I am directing a lot of my spend to the SYW card. Getting 10% back on GGR purchases through December and each month I have been getting 10% back on internet spend. Working on stacking with organic spend for 20% back.

The $2.5k cap is somewhat annoying to manage on the BoA CCRs.

One viable end-game single card setup would be the BoA Premium Rewards card. 3.5% on travel & dining, 2.625% on all else. Blended, probably something like 2.8%. Not bad for a single-card setup.

Robinhood has the 3% card, but I would prefer not dealing with RH.

I enjoyed the video :). Definitely a bummer to get the letter today. I thought it would take much longer for them to turn on the “grandfathered” customers but I guess not. I really enjoyed the card, it was simple, never declined, no hassle, and I even went in person for a bank transaction with the savings account (sold a car, deposited check) and US bank was pleasant. So sad and frustrating.

I will definitely move the investment account, they dont deserve to custody that, but is it worth it to open and fund the checking 10k to get 2.5% back? I have not heard anyone mention that but the math to me says it would be worthwhile. Hoping to find another 3%+ simple card again soon.

Glad you liked the video. It really hit home after watching the US Bank debacle.

I think you bring up a really good point about the 2.5%, which is almost as good as BoA’s 2.625% (which requires $100k of assets).

The other option is the RH 3% card, but then you’d have to deal with Robinhood (and pay ~$50/yr for RH gold).

I’m not sure what I’ll do yet…

I got the “bad” letter yesterday. Oh well, I guess it’s back to Alliant (2.5%) for me.

Reading through the discussion on Bogleheads, there seems to be a chance that the two separate letters was a mistake, and the investment account will still qualify for everyone. It’s funny that people have so little confidence in US Bank that this is considered a reasonable possibility.

In addition to everything else, I find it strange an annoying that the notice came via regular, mail, and not an email. I only opened the letter because I saw the discussion online and expected it–otherwise I probably would have just thrown it away. But not long after opening it, one of my kids cleared off the counter and threw it away, so now I can’t go back and refer to it.

Sorry for dragging you into this mess!

Alliant is changing their card to 1.5/1.6%

I hadn’t heard that! Crap! Do you have a link?

nerf-pocalypse

https://www.reddit.com/r/CreditCards/comments/1lvvxnv/alliant_visa_signature_moving_from_25_to_16/

My wife and I have both been on the waitlist for the 3% RH card since they announced and nothing, so I’m somewhat skeptical if it will still exist when/if our names are ever selected for the “privilege” of applying!

Same here, but a reader emailed me yesterday to say he was just approved for the RH card after the Smartly nerf. All he had to do was email/chat to inquire. He too was on the waitlist from day 1.

Crazy! That didn’t work for me.

Bummer!

I use the RH Gold 3% card, use it for almost everything. Use the 5% category citi custom cash card for gas and my wife uses her citi custom cash 5% category on groceries. Pretty simple and efficient system. Only thing I occasionally screw up is accidentally using the RH Gold for gas without thinking about it. $50 annual fee on RH Gold, but I was already paying that before getting the card for retirement match.

Pretty slick. I think many are going to jump ship to Robinhood now.

This may be redeemable if the transfer partners are good. Otherwise, I’ll likely downgrade to Connect, Cash+, etc.

Citi has a really good setup right now. They added American Airlines as a transfer partner with their new premium card (Strata Elite, though you only need that or the $95/year premier card) to transfer to them. There can be really good value, but everyone is predicting there will be devaluation of AA miles as a result. Citi’s Strata card is very good for a no annual fee card and I utilize my multiple Custom Cash cards.

Thanks for the input!

And the American Centurion Card enters the room. @FP, you really need to fix the comment nesting.

ChatGPT finally helped me solve nesting! Thanks for the kick in the pants; it was on my list of things to do for a while now.

It would also be extremely helpful if your posts included a date!

Ran across this from CFBC but since we are in a shutdown and I’m not sure the agency exists anymore.

https://www.consumerfinance.gov/compliance/circulars/consumer-financial-protection-circular-2024-07-design-marketing-and-administration-of-credit-card-rewards-programs/?

Seems like a long shot… but I agree with your frustration.

So you’re planning on moving your investments out of US Bank? I got the “good” letter and while I’m not happy about it the 4% back on $10k a month is well within my typical spending. That makes me think the card is worth using until the terms further deteriorate.

Having received the “good” nerf letter, I’ll leave the $100k there until they nerf the card completely. My guess is 6 months.

I loved this card for the simplicity of only having one card. I’ve considered the BoA strategy, but I’m not sure I’m as dedicated as you.

I really wish Fidelity would revive their Rewards+ program and give something at least as competitive at the 2.625% at BoA.

Maybe I should just give in and do the brokerage transfer game.

Join the BoA cult. It is not nearly as bad as I’ve made it seem.

For starters, do the Premium Rewards card. 3.5% on travel/dining, 2.625% on all else. $95 annual fee is offset by $100 travel credit if you do $100 at United Travel Bank (basically a gift card to yourself) or AA egift card.

If I were less psychotic, I’d do that for a blended cash back of ~2.8% or whatever. Not bad at all.

Regarding the bonus transfer game, I’d recommend it if you can stomach a bit of busywork.

It seems the sustainable thing (assuming you’re not always chasing sign up bonuses) is to use 5x cards as much as possible and then complement with a 2%+ card.

Agreed, or better yet 5.25% and 2.625%, which was my strategy before I got involved with US Bank

Yes, you certainly had a good one. I think you were putting more on the Premium Rewards than you needed to but the simplicity is certainly there.

There is one more advantage of 5x cards like the Chase Freedom (Flex) card or Citi Custom cash and that is they earn points not just cash. Depending on how the points are used, they can be worth more than 1 cent each, so the earnings can go up considerably. Consider the Chase Freedom example where you are getting 5x on the quarterly category for up to $1500 per quarter (real numbers). That means you can earn 7500 Chase Ultimate Rewards points. One of the most popular partners here is Hyatt and those points are frequently worth about 2 cents each. So, one could potentially earn 10% on those purchases. It doesn’t really work that way though, because you may not have been willing to pay Hyatt’s rate, so you may have stayed at a hotel that was $80/night instead of $100/night. However, you can see how you do better than just 5.25%.

Just curious, let’s ignore the bait and switch for the moment.

If someone else comes out with a card with the “good version” of the current terms at the outset, would that be a card that you would find desirable?

I.e. 2% cash back, no annual fee, 3% FTF.

If you park $100K combined in XXX-brand checking/savings/investment accounts, you get an added 2% cash back (=4%) up to $10K spend, but excluding education, tax, gift cards, insurance, B2B, and third-party bill payment from the bonus (still gets base 2%).

Parking $5K would give 2.5% and 50K would be 3%.

I’m not disappointed to have gotten the “good” nerf letter.

I’m disappointed in their bait and switch tactics and have no confidence the “good” terms will persist more than a few more months. I’m disappointed that I recommended the card to friends/family for them only to receive the “bad” nerf a few weeks later. I’m disappointed in the junk show that is US Bank (hilarity in their bungling of the situation, terrible brokerage which encourages transmitting sensitive docs over unsecured email, etc).

But I’ll continue to milk the 4% for another few months until they nerf us all.

So, until they nerf you more (a strong assumption admittedly), you’ll continue to do business with them, but if someone else offers similar/identical terms, you’d move in a heartbeat, and plan to never do business with USBank again?

Your level of anger/spite/disappointment hasn’t risen to the level where you’re moving your investments proactively?

I note that the Fidelity card is run by Elan, a subsidiary of USBank….

I’m pretty sure that the “good” terms would work for many people out there as a great single card setup, albeit people who don’t also suffer from overoptimization-itis. 😉

I’m not sure which is a stronger assumption:

* The perpetuation of the “good” terms for many years, or

* The rapid demise of the card for all users

Given the junk show over the past several months, I think the former is a stronger assumption than the latter, but we can agree to disagree here.

Do I think people with the “good” nerf should preemptively cancel? Nope, obviously not. The fixed cost has already been incurred and the gravy train is flowing, albeit a bit slower now. I didn’t think it necessary to state explicitly in the article, but maybe that was an oversight.

Do I regret getting the card? Conditional having received the “good” nerf, no. Do I regret recommending the card? Conditional on my friends/family having received the “bad” nerf, then yes — it made me look like an idiot. It was clearly not worth the hassle for a couple months of 2% excess rewards vs a 2% card (or even less vs BoA’s 2.625%/5.25% setup).

Regarding Fidelity/Elan/USBank, I don’t have any qualms with Elan being an administrator of the card. I’ve had permutations of that 2% Fidelity card since 2005 and have never had a single issue.

I just think that US Bank deserves a bit of flak for the botched rollout of this (obviously unsustainable and much-hyped) card. It is as bad as I’ve seen in my life by a decent margin.

“Do I regret recommending the card? ….. it made me look like an idiot.” I just fell for the bait and switch from a “wealth management” banker. I set up the smartly accounts that put me into the premier category and with his assurance I was all set for 4% I setup autoay of a few bills and went on a 6 week vacation – using the card exclusively – low and behold I earned wonderful credits for the monthly fees for the accounts (which I would never pay for for any bank) 2% on my credit card charges a whole1 dollar reward! I called the credit card company and they said – oh it just hasn’t kicked in yet until after your first statement…. When I look online it says a meet the qualified amounts… Called again after the statement and they transfer me and then drop the call. THEY SUCK. Called the wealth management banker about it – he basically said he’d look into it and moved on to to talk about my moving my brokerage account over? comedian! Good thing I didn’t move it before. I told him to solve the issue or our converstaion will be about closing my accounts. I won’t do business with a company that pulls this kind of crap. He led with the 4% … Even now the web site still shows me as qualified. There really should be a class action suit filed against them. BLATENT BAIT AND SWITCH! Oct 2025

Sorry about the terrible experience.

Random card that gets no attention, but is a pretty good card for many would be…

https://www.breadfinancial.com/en/bread-rewards-credit-card.html#accordion-9fd398f1f7-item-bcfb6d5924-button

Bread Amex 3% on gas, grocery, restaurant, and utilities. I still prefer the Mesa Homeowner’s card, but that is because the mortgage bonus winds up making it a VERY good card. That being said, the Bread Amex has no annual fee and no FTF. This compares pretty well to the Capital Ones Savor card, unless you are going to transfer to partners with Venture. The Bread card is unusual in offering a 25% bonus for 20+ transactions/month.

I hadn’t heard about either card. Thanks!

Did you see the 6% BOA CCR offer for one year. I suspect BOA offered this promotion to blunt the US Bank Smartly credit card offer. If you have >$100,000 assets with BOA and you pick a qualifying category, you get 8.25% back on your purchases. If you have an executive membership at Costco and purchase a shop card online with this card you get 10.25% back on your Costco purchases. After one year you lose the extra 3% and it converts back to a regular BOA CCR card. Between my wife and myself, this is our 5th BOA CCR card. Not bad for a limited time offer.

Really nice offer! I had seen that and was kicking around the idea of doing it. We’re up to 8 CCRs so not sure if BoA would sign off on a 9th…

With Smartly dying a miserable death, I’m thinking about opening up the Premium Rewards card again (or Elite if I don’t mind a few more hoops).

Continuing this ‘fun’ journey with US bank smartly accounts, i just got a letter today by snail mail stating that they have the authority to decide who gets the savings boost rate for Smartly accounts, and i am effective sep 11, no longer eligible for the better smartly savings rate and will instead receive the basic variable 0.05% rate! What gives? Getting better by the day!!

The train wreck continues!

Great Article, you really captured my outrage and lol on the Michael Scott Golden ticket thing. I’ve been busy with life and missed all of this until I realized I was only earning 2%. I guess I got the bad letter.

I love the username!

One silver lining that you might find interesting is that those of us who received the “good nerf” have seen a reduction in rewards to 2% but apparently we’ll get the extra 2% at statement close. My statement closes in about a week, so I can’t test that theory until then. I guess I’m not holding my breath for a favorable outcome…

Thought that I was in the brokerage would still count camp as I had v1. When my 4% did not reset for this month, I called in and, sure enough, brokerage no longer counts. What a joke … card went from the best to one of the worst. I had not done BOA … but looking to US Bank brokerage to Merrill and get one of BOA’s cards. Fortunately, none of my friends that I recommended US Bank smartly card went with it – they thought it was too big of a pain to be setting up checking, savings, and transferring $$ into a brokerage account. Yikes … would hate to be the person at US Bank that thought up this fiasco and handled its demise so poorly.

My statement closes tomorrow at midnight, so I guess I’ll see if the party is over then.

My card transitioned from 4% to 2% on 9/17, but the prevailing rumor is that us grandfathered people would be made whole with the full 4% at statement close. I’m about 36 hours away from being able to prove/disprove that theory.

To close the loop, I’m still getting 4%. I confirmed it with my recent statement close. “Good” nerf here. $100k in brokerage.

What do you think about the elite money market account ? It’s so frustrating- because I thought I was finally going to be able to get the 4% by putting money into elite money market account however, apparently you can’t have a savings account open with them. But I think the 4.25% is still worth it. Just waiting to see how quickly they will change that as well!

I hadn’t heard of the elite money market account until this comment. I just looked it up.

Having $25,000 earning ~zero interest is a non-starter for me.

My Fidelity cash management account set up earns me the most competitive rate in the country and takes no work to maintain. https://frugalprofessor.com/the-ultimate-guide-to-fidelitys-cash-management-account-cma/

Going forward, I hope to do as little business as possible with US Bank and is much business as possible with Fidelity.

I signed up for the US Bank Cash+ card for the sign-up bonus intending to product change to Smartly but missed the window. If you get totally nerfed on Smartly, you might find value in product changing to Cash+ for 5% back on utilities and gym memberships, which BofA CCR doesn’t offer.

Thanks for the suggestion!